The Stock That Tripled While Nobody Was Watching — And Why I Haven’t Bought It Yet

LSE Main Market • Industrials / Electrical Equipment

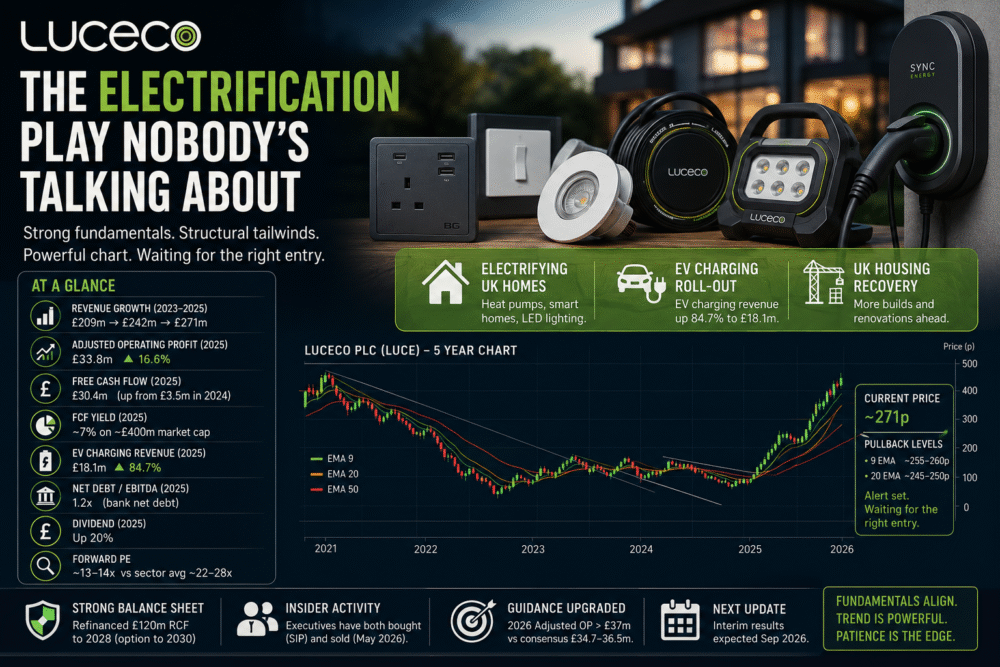

Price: ~271p • Market Cap: ~£400m • Verdict: WATCHLIST — Alert set at 255p

Right, let’s talk about Luceco. Not the sexiest name on the LSE. Doesn’t have the narrative punch of a defence stock or the headlines of a housebuilder. But the chart doesn’t lie, the numbers are genuinely good, and if you’ve been watching UK mid-caps lately this one has been quietly doing something very interesting.

What Does It Actually Do?

Telford-based, founded 1941, LSE Main Market. Luceco designs and manufactures electrical products — wiring accessories under the BG Electrical brand, LED lighting, cable management, portable power, and increasingly EV chargers through their Sync Energy brand. Market cap around £400m. It’s not a household name but its products are in most households. Every switch, socket, extension lead, and EV charger going into a British home or commercial building is a potential Luceco sale.

The UK is the engine room — roughly 80% of revenue comes from domestic customers. The rest is split across Europe, Middle East, Americas, and Asia Pacific.

The Numbers — What’s Happening Here

This is where it gets interesting for a swing trader who cares about fundamentals backing the technicals.

Revenue has grown from £209m in 2023 to £242m in 2024 to £271m in 2025. That’s not explosive growth but it’s consistent and accelerating. More importantly, adjusted operating profit has gone from £22m to £23m to £33.8m over the same period — a 19% compound annual growth rate over three years. The business isn’t just growing the top line, it’s getting more efficient as it scales.

Gross margins tell the same story. Back in 2022 they compressed badly to 33% — post-COVID cost inflation hit them hard. They’ve rebuilt all the way to 42.4% in 2025. Better than they were before the storm hit.

| Metric | 2023 → 2024 → 2025 |

| Revenue | £209m → £242m → £271m (+11.9%) |

| Adjusted operating profit | £22m → £23m → £33.8m (+16.6%) |

| Gross margin | 39.6% → 40.2% → 42.4% |

| Adjusted EPS | Up 20% in 2025 to 15p |

| Dividend | Up 20% to 6p full year |

| Free cash flow | £3.5m (2024) → £30.4m (2025) |

| EV charging revenue | Up 84.7% in 2025 to £18.1m |

Free cash flow bounced back strongly to £30.4m in 2025 from £3.5m in 2024. The 2024 number was artificially depressed because the Red Sea disruption forced a big inventory build that ate cash. In 2025 that unwound and the true cash generation of the business came through. On a market cap around £400m, that’s a free cash flow yield of roughly 7-7.5%. Not extraordinary, but solid for a business growing at this rate.

EPS up 41% in 2025. Dividend up 20%. Share buybacks ongoing. The capital allocation is disciplined.

Is It Cheap?

Forward PE of 13-14x for a business growing adjusted operating profit at nearly 20% per year with 20%+ return on equity. The peer average in the European electrical sector sits at around 28x. Even the UK peer average is around 22x. Luceco trades at a meaningful discount to both.

The PEG ratio is 0.37 — anything under 1 suggests a stock is cheap relative to its growth rate. ✅

After the Q1 2026 update in mid-May, company-compiled consensus for 2026 adjusted operating profit moved to £38.3m, with a range of £37.7m to £40.5m. That is a management team consistently beating their own guidance and watching analyst estimates chase the stock higher. Pay attention when that pattern develops.

Forward PE ~13-14x vs European sector average ~28x. PEG 0.37.

Either the market is wrong, or there’s a reason for the discount. The China manufacturing risk and Americas headwind are part of that story — but it still looks cheap relative to the sector.

The Debt Picture — Always Worth Knowing

Bank net debt stood at £52.3m at the end of 2025, with net debt at £59.9m. Bank net debt to EBITDA at 1.2x — comfortably within their 1.0-2.0x target range. They’ve just refinanced a £120m revolving credit facility running to May 2028 with an option to extend to 2030. No near-term financing risk.

Interest costs have jumped from £1.6m in 2021 to £6.9m in 2025 — the cost of the acquisitive growth strategy. Worth keeping an eye on if rates stay higher for longer. It’s not a problem today but it’s a number to watch.

Insider Activity — The Full Picture

On the buying side: Chairman Jonathan Hornby bought £120k of stock in April 2025 at around 120p.

CEO Pim Vervaat and CFO Will Hoy both bought in November 2024.

Those purchases at much lower prices are a matter of record and they were genuine conviction buys.

However — in May 2026, CEO John Hornby sold 1,000,000 shares at 268.52p and Chair Giles Brand sold 475,000 shares.

That is material director selling at current levels and needs to be disclosed, not ignored. It doesn’t kill the thesis but it does require an honest question: if the stock is as cheap as the numbers suggest, why are the people who know it best selling near the highs?

One possible answer: they bought at 120-135p and this is normal profit-taking after a near-tripling. Another answer: they see the extension in the share price and are reducing at what they consider fair value. We don’t know which. But you should know the selling happened.

Institutional ownership remains solid — 51% institutional. BlackRock in at 10.4%, Janus Henderson, JPMorgan, Hosking Partners all present. The big money knows this stock exists.

Who’s Competing With Them?

Worth knowing the landscape, because it actually makes Luceco look better not worse.

The global heavyweights in this space are Legrand, Schneider Electric, Siemens, and ABB. French and German industrial giants with market caps in the tens of billions. Legrand is a formidable competitor particularly in the wiring accessories segment — but it trades on a completely different valuation, is listed in Paris, and is a very different beast for a UK swing trader. Schneider Electric is the same story.

The point is — Luceco isn’t trying to compete with Legrand globally. It dominates the UK trade channel. BG Electrical is one of the most recognised wiring accessory brands with UK electricians. That’s a defensible position that the French giants don’t easily disrupt.

The more relevant comparison is the valuation gap. The European electrical industry average PE sits at around 27.9x. Luceco trades at 17-18x trailing. That’s a 35-40% discount to its sector peers for a business growing faster than most of them.

Luceco’s vertically integrated model with significant manufacturing in China gives it a cost advantage and supply chain control that lets it compete aggressively on price in the more commoditised segments. The flip side is tariff and geopolitical exposure — management have been navigating it well but it remains a real risk, particularly with US tariff policy unpredictable.

Luceco isn’t going to take on Schneider Electric. It doesn’t need to. It owns the UK trade channel, it’s building out EV charging before the big boys have fully committed, and it’s doing all of this at a valuation that doesn’t price in much success. That’s the opportunity.

The Sector Tailwind

This sits at the intersection of three structural UK trends that aren’t going away.

- Electrification of UK homes — every heat pump, EV charger, and smart home installation needs wiring accessories and LED lighting. This is a decade-long cycle, not a quarter.

- The EV charging rollout — EV charging revenue grew 84.7% in 2025 to £18.1m. Small in absolute terms but compounding fast and Luceco has first-mover advantage in the UK trade channel.

- UK housing — planning reform, rate cuts, and the government’s housebuilding targets mean more homes getting built and renovated. Every single one needs what Luceco sells. They’re not a housebuilder but they’re a direct beneficiary when housebuilder activity picks up.

None of these tailwinds are going away in a quarter or two. That’s what makes the fundamental case compelling even if the entry timing needs to be right.

Recent News — The Clean Version

| Date | Event |

| 25 Mar 2026 | Full year 2025 results — revenue £271m, profit up 16.6%, dividend up 20%, guidance upgraded above consensus |

| Mid-May 2026 | Q1 2026 trading update — revenue up ~11% organic, margins healthy, strong start to year confirmed |

| 27 May 2026 | Director selling RNS — CEO sold 1m shares at 268p, Chair sold 475k shares. Needs monitoring. |

| 27 Apr 2026 | Market purchase of shares for EBT — company buying stock for employee share schemes |

| Sep 2026 (expected) | Half year interim results — this is your RNS blackout window to be aware of |

No profit warnings. No placings. No debt covenant issues. The fundamental news flow has been clean. The director selling in May is the one item that deserves ongoing attention.

The Chart — What the Technicals Are Saying

The Weekly Chart

The long-term context matters here. This stock peaked around 500p in 2021, then had a brutal multi-year downtrend all the way to around 65p by late 2022/early 2023. That’s an 85% drawdown. Then it ground sideways for nearly two years between roughly 100-200p with all three EMAs flat and tangled. Dead money for a long time.

Then from late 2025 it launched. The weekly EMAs are now in perfect traffic light order — 9 EMA (green) above 20 EMA (amber) above 50 EMA (red), all pointing aggressively upward. This is a stock that has woken up after years of doing nothing. The weekly structure is genuinely bullish. Weekly RSI has pushed above 70 — which confirms real momentum but also flags the weekly timeframe is extended.

The Daily Chart

From the October 2025 low at around 110p to the recent high of 286p is a near-tripling in six months. The move is clean. EMAs in order throughout. The descending channel that capped the stock for most of 2024 and early 2025 has been convincingly broken and left well behind.

The 9 and 20 EMAs on the daily are rising steeply. The 50 EMA (red) is still sitting around 200-210p — price is more than 30% above its own 50-day average. The ATR has spiked. Daily ranges are elevated. This is not a quiet, compressing setup ready for a clean entry.

This is extended. It’s a great trend but it is not a clean entry right now. Chasing a stock 30% above its moving averages after a near-tripling is exactly the kind of trade the plan exists to stop you making.

What I’m Watching For

The setup I want to see is a controlled pullback to the 9 EMA on the daily — currently around 255-260p — on declining volume. Volume drying up on the pullback tells you it’s a healthy breather rather than distribution. Then a green confirmation candle at or above that level. That’s the entry signal.

A deeper pullback to the 20 EMA around 245-250p is also valid and gives slightly better risk/reward with a tighter stop below it.

| Scenario | Action |

| Pullback to 9 EMA (~255-260p), volume dries up, green confirmation candle | Run full checklist. If all green — enter on open of next candle. Stop below the EMA. |

| Deeper pullback to 20 EMA (~245-250p), same conditions | Slightly better R/R. Same process. Tighter stop. |

| Continues straight up from here without pulling back | Do not chase. Watch it. There will be another entry. |

| Breaks below 20 EMA on daily with volume | Thesis weakening. Remove from active watchlist. Reassess. |

| Negative RNS before entry | Do not enter regardless of price level. Wait for clarity. |

Alert is set at 255-260p. When it gets there I’ll run the full checklist — EMAs, RSI, volume, ATR, RNS calendar — and reassess. Until then this sits on the watchlist.

The Bottom Line

Luceco is a fundamentally sound, cash-generative business riding genuine structural UK tailwinds, trading at a significant discount to European sector peers. The chart trend is powerful. The weekly structure is as clean as anything on the LSE right now.

The caveats are real — the stock is extended, the director selling in May needs watching, the China manufacturing exposure is a genuine risk, and the Americas headwind hasn’t gone away. None of those are reasons to ignore it. They’re reasons to be disciplined about the entry.

It just needs to come back to me before I go near it.

Missing the entry costs nothing. A bad entry at 271p into an extended move could cost 15-20% before the trend reasserts. Those are not equal outcomes.

Watchlist. Alert at 255p. Patient.

Omera Trading • Not financial advice • I’m a bloke with a spreadsheet and an internet connection, not a financial advisor • Always do your own research