During the covid pandemic Square Capital CEO Bill Ackman, a knowledgeable individual with years of experience in the stock market, appeared on CNBC to inform us that the world was doomed, every business in the hospitality industry was certain to go bust, and we should sell everything now, it was a comment hard to ignore. Later we found out Mr Ackman had short positions. Was this because he truly believed his theories, or was it to make a quick buck by scaring the investment community, thus driving the stock prices down as he closed the position soon after making millions? The hospitality sector bounced back with the rest of the market in a V-shaped recovery.

More recently, many analysts dressed in suits with numerous letters after their name told us that crude oil was certain to reach $100+ a barrel in the coming weeks after OPEC cut production. How can I, a lad from Yorkshire with 4 Ds in eight GCSE subjects, none of them economics, argue with someone so intelligent confidently giving me their economic predictions when I have a different view based on technical analysis and arguments for a recession showing that oil will struggle to reach those highs. Crude Oil is down 15% this week to $68 per barrel.

Nine times out of ten, predictions on TV and in the media are absolutely nonsense and are proven wrong time and time again. The one that gets it right has a movie made about them, such as ‘The Big Short’ with Michael Burry adopting some god-like status with investors hanging off his every word. They ignore the numerous times he is wrong.

As you can see from the companies I talk about this week, the media always has some view of what you should be doing, but I say ‘stick to your lane and have the confidence to have a different view from the suits’. There is no right answer to the randomness of economics. The best traders I follow state their trading improved once they turned the TV off.

CARD FACTORY

Like many other retailers, Card Factory faced significant challenges during the COVID-19 pandemic. In the early stages of the pandemic, the company was forced to close its stores temporarily as part of the UK government's lockdown measures. This resulted in a significant decline in sales and revenue for the company.

Some say Card Factory was slow to pivot its focus onto online sales channels and offset some of the losses from its physical stores. The company eventually invested in its e-commerce infrastructure and expanded its online product range to meet the increased demand for home delivery during the pandemic.

Despite these efforts, Card Factory's financial results for 2020 showed a decline in revenue and profits compared to the previous year. The company ran into financial stress, which at one point, looked like the business would struggle to continue trading.

I became highly bearish on the company at this time, especially after talking to members of staff who confirmed the slowing of sales and no improvement. Since then, the management has learnt from their mistakes and turned the company around, especially the leaving CFO Lee…… who appears to have turned the company's financial situation around and secured new credit facilities.

I should have done better on Card Factory. I had a bearish bias, stopped researching the company, and missed the turnaround. The share price has been up nearly 200% since September 2022, and I only realised this recently. We always continue learning in trading, and in the future, I will keep a closer eye on companies that interest me until they delist from the stock market.

Who is Card Factory?

Card Factory is a UK-based retailer that sells greeting cards, gifts, and party supplies. The company was founded in 1997 and has since become one of the largest card and gift retailers in the UK, with over 1,000 stores nationwide. It is hard not to see a store when visiting any town centre or retail park.

In addition to greeting cards, Card Factory offers a wide range of products, including gifts, balloons, party supplies, wrapping paper, and seasonal decorations. The company prides itself on providing high-quality products at affordable prices, and its products range from fun and light-hearted to sentimental and heart-warming.

My family and I often use Card Factory for birthday gifts, decorations, and cards, mainly in a last-minute rush favouring the diverse range of products and low prices.

The Business Model

Card Factory's business model provides customers with a wide range of affordable greeting cards, gifts, and party supplies through a network of physical stores and an online store. The company's business model is centred around the following key elements:

Wide range of products: This allows the company to cater to a diverse customer base and appeal to different tastes and preferences.

Low prices: Card Factory's products are designed to be affordable, with the company's pricing strategy focused on offering value for money. This helps the company to attract price-sensitive customers and differentiate itself from competitors.

Multiple sales channels: Card Factory operates through a network of over 1,000 physical stores across the UK and an online store. This allows the company to reach customers through multiple sales channels and cater to shopping preferences.

Personalisation: Card Factory offers personalised cards and gifts, allowing customers to add photos and messages to create unique and thoughtful presents for loved ones. This provides an additional revenue stream for the company and helps to differentiate it from competitors.

Efficient supply chain: Card Factory's efficient supply chain allows it to manage its inventory effectively and minimise costs. This helps the company to maintain its pricing strategy and profitability.

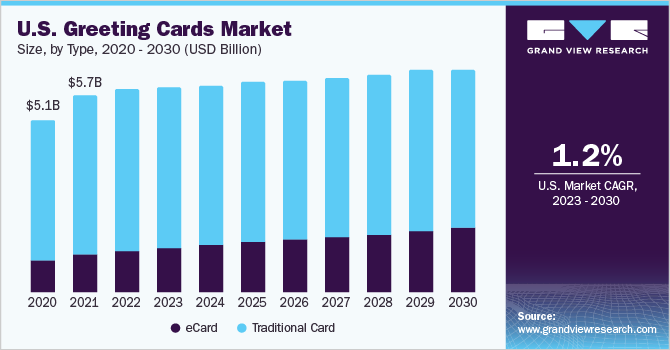

The global greeting cards market was valued at USD 19.25 billion in 2022 and is expected to expand at a compound average growth rate (CAGR) of 1.2% from 2023 to 2030. The increasing popularity of festive celebrations and occasions drives the growth of the greeting card market. Industry growth was suspected to decrease with the development of the internet, but this is not the case to date. Many still see the greeting card to show someone you care, and I see this tangible product performing this task better than any email. Recently, many have been worried about the cost-of-living crises affecting sales, but I go against the crowd with my opinion. Card Factory is not a cyclical business but more in the staple category, Card Factory sells products to put a smile on someone's face at very low prices, and these smiles will continue through any recession, maybe more so.

How's Current Trading

Brilliant! The company is bouncing back, with revenue up 27.7%, for FY23. Margins are improving, inflation and other costs are managed well, and the banks are happy that Card Factory is paying them back with debt decreasing to £57.2 from 74.2 in 2022. This was helped with Free Cash Flow (FCF) of £91m. Under the financial restrictions on the loans, the company cannot currently pay dividends but suspect it will not be long before these can return.

The outlook remains positive for the year ahead, and the company is on track to deliver their 'Opening Our New Future' strategy. This strategy has the ambition to build upon dominance within the UK card market and to become the leading, technology-enabled, omnichannel retailer in the sector, hoping to achieve revenues of around GBP650m in FY27. I am confident that the company can accomplish this.

With a quick look through the 2023 financial results, I may not have missed the full recovery of Card Factory, and there's much more upside to come, so I will conduct more research before investing in the company.

A Quick Price Target

As previously stated, Card factory was severely impacted by covid, which caught the management team off guard. Since then, things have been recovering, and the normality of pre-covid can be seen in trading. I will base my valuation on this.

The average revenue growth pre covid from 2016- 2020 was around 5%. So, I use this for my price target for revenue, with FY24 coming in at 486.84m, roughly around the same as analyst estimates.

Analysts, however, estimate a strain on operating margins reducing the Earning Per Share (EPS) to 11p. I take a different view. Energy and supply chain costs are down, and inflation is due to fall and, hopefully, interest rates (I may be over-optimistic with that one for FY24). The management is handling all cost pressures well and learning from previous mistakes. With this, I estimate an EPS of 16p based on slightly higher operating margins.

The price-to-earnings ratio pre-covid sat at an average of 13.5 since 2015. As I witness a normalisation of trading in the shares of Card Factory, I am happy to value this company on a PE of 13.5x, and this gives me a price target for FY24 of 216p on the bull side and 148.5p on the bearish side which factor in analysts’ expectations on declining or flat operating margins.

BARRATT DEVELOPMENTS

Barratt Developments gave us a Trading update this week, and confidence is returning to the UK Housing Market. The company can meet full-year 2023 expectations and has increased its order book. The 6.7% dividend yield looks safer than it was six months ago, and this could be an opportunity to invest in a house builder rather than buy-to-let, where the average yield is around 4%.

I have confidence in the house builder and wish I owned more of them for the attractive dividends and capital growth they offer. The only house builder I own is Gleeson (GLEE).

BDEV is up nearly 65% from its lows in October 2022, where it formed a double bottom in price (A double bottom is a type of price movement identified in technical analysis where there is a fall in price led by a gain and then another drop and finally, a price rise which commonly continues up).

When the price hit bottom, I was tempted to get involved with my favourite builders. Although I advocate investors not to be influenced by the media, I am ashamed to say I was. It is hard for anyone to ignore experts shouting from the rooftops that an imminent market crash is approaching. Looking back with hindsight, after there was no crash (well, not yet). The risk wasn't ever there. Prices in the housing market have only inflated with inflation; the housing prices in real terms, excluding inflation, have not raised as much, dismissing the case of a bubble. The only last housing market bubble we saw was pre-2008.

Housing Market Bubble

With the disastrous results in regional elections for the conservates this week, many housing investors are waiting patiently for the subsequent government intervention to inflate prices to make their voters happy and price out the vulnerable trying to get a foothold on the ladder—interventions such as Help-to-buy.

A housing market bubble refers to a situation where the price of housing in a particular area or country rises rapidly and significantly beyond its intrinsic value. The United Kingdom experienced a significant housing market bubble in the mid-2000s, which peaked in 2007 and burst in 2008.

During the bubble, house prices rose rapidly, with many people purchasing homes to invest or flip for a profit. The main factors that led to the bubble included low-interest rates, lax lending standards, and easy access to credit. The government (Labour in this case) we're happy they could secure votes from a prosperous public. These factors encouraged many people to take out large mortgages and buy homes they couldn't afford, leading to an oversupply of housing.

The bursting of the housing market bubble in the UK had significant consequences, including a decrease in consumer confidence and a substantial rise in mortgage defaults and repossessions. Many people who had purchased homes during the bubble found themselves owing more than their homes were worth, leading to financial distress and negative equity. I, too, fitted into that camp in 2008, losing nearly 30% of equity after my purchase six months prior. We live and learn.

Supply and demand will always meet in the middle in a lesser fair economy with no government intervention. I believe bubbles, especially in the UK housing market, are created by governments seeking votes from a public obsessed with housing prices.

Help to Buy!

On the face of it, help to buy looks like a policy to help people get on the housing ladder but can have the opposite effect by inflating prices higher, thus making it harder for first-time buyers. If this policy is reintroduced, the share prices of the housebuilders such as Barratt will increase, but this 'intervention' and many like it will just support the next housing bubble. The only way to succeed in this industry is to know when not to buy property, and it's easy to spot.

I want to trade a UK House Builder Exchange Trader Fund (ETF), but there isn't one. Instead, I want to start positions in Taylor Wimpey (TW.) Persimmon (PSN), Barratts (BDEV), and buy more Gleeson (GLEE).

WICKES

Wickes is a British home improvement retailer offering a wide range of products and services for DIY enthusiasts and professionals. The company has over 200 stores across the UK.

Wickes offers a variety of products, such as building materials, flooring, doors and windows, electrical and plumbing supplies, kitchens and bathrooms, tools and hardware, and much more. In addition to its products, the company also provides installation services for kitchens, bathrooms, and wardrobes.

The company aims to provide customers with high-quality products at competitive prices. Its stores are designed to be easy to navigate and offer a helpful and informative shopping experience.

Wickes was first listed on the London Stock Exchange in August 2021. Before that, it was owned by Travis Perkins, a British builders' merchant, and was part of its consumer division. However, Travis Perkins decided to spin off Wickes as a separate entity and offer shares to the public.

Wickes interests me because I own Grafton and Kingfisher. I reported on Grafton on the 3rd of March, 2023. My main decision was to invest in the home improvement/ DIY sector because I saw the demand around me. I regularly use Selco (Grafton), Screwfix, and B&Q (Kingfisher) and witness the stores' busyness.

All three companies have a positive outlook and see trading and inflation returning to normal. I have many friends investing in their properties, and just today, I tried to book someone to fit me a patio door, and I was told they could only fit me in at the back end of June. Where is this cost-of-living crisis?

As I am already invested in Grafton and Kingfisher, I will not be getting involved with Wickes. Still, the company is very attractive due to the capital gains from the pent-up demand and the 5.77% dividend yield.

Estimates for FY23 are an EPS of 17p, raising to 22p for FY25. I like to value companies on a PE/investor sentiment ratio; this fits my short-term swing trading strategy. If I were a long-term investor, I would look at discounting future cash flows for a longer-view price target.

Wickes was only listed on the UK stock market in 2021. I need help understanding what investors and traders would be prepared to pay for the company in different economic environments; Travis Perkins has had an average PE ratio of 13x since 2013. Today Wickes trades on a Price to Earnings ratio of 8.7x. It did rise to nearly 12x soon after listing, but these crazy times of 2021 are something I ignore.

At today's PE of 8.7x, my price target would be 191p by 2025. I calculate this using analyst estimates which are very bearish on the industry. If the economic outlook improves, the earnings estimates will be revised substantially, and investor sentiment will follow. There could be some excellent upside from here if you believe in a bright future and not the depressive recession headlines, we are bombarded with daily.

ADVANCED MICRO DEVICES

I have always watched Advanced Micro Devices with some interest, watching them perform better than their most significant rival intel, something many would not have predicted some years ago.

Most chipmakers' stock is currently struggling due to the fall in the PC market, but this is a small blip on a huge horizon. The PC market went crazy during the pandemic with the new working-from-home culture. Many of these PCs and laptops purchased have a lifespan of around three to four years, so we could see much demand going forward. The CEO Lisa Su's comments backed up this theory, "We believe the first quarter was the bottom for our client processor business".

Despite this outlook and an overall beat on Revenue and EPS, the stock price was down 9% on Wednesday.

- EPS: 60 cents per share adjusted vs. 56 cents per share expected

- Revenue: $5.35 billion vs. $5.3 billion expected

The 9% drop was short-lived with the announcement that Microsoft plans to collaborate with AMD on a new A.I venture. This year, A.I. is the new buzzword; it joins 3D printing, Crypto, Electric Cars, Cannabis, and many more that may fizzle out to nothing.

Will I get involved?

I'm not too fond of the dilution of the AMD share price since 2015, which has doubled and with the rise in the pound against the dollar, this will affect any purchase of stock I make. But I am happy to add this to my short-term trading watchlist that uses spread betting. Spread betting comes with higher costs if holding overnight (especially in a high-interest rate environment), so I use this very short term. I look at trending stocks and entering on a 1-hour timeframe when I identify a pattern. With the fundamentals due to improvements in the chip sector and the introduction of the US chip act funding $39bn to build advanced semiconductor manufacturing capabilities, we could see some momentum enter companies such as AMD.

DISCLAIMER: I am not a financial advisor; this is not a financial advice website. All information provided does not take into anybody’s personal circumstances, situation, trading style or risk levels. If you are making an investment or other financial management decisions and feel you need guidance or advice, please consult a suitably qualified licensed professional. If interested in trading, please develop your strategy and research your own trades.

{kind=link}

{kind=link}

{kind=link}

{kind=link}